Mortgage Investment Corporation Fundamentals Explained

Table of ContentsIndicators on Mortgage Investment Corporation You Should KnowAbout Mortgage Investment CorporationThe Greatest Guide To Mortgage Investment CorporationMortgage Investment Corporation Fundamentals Explained5 Easy Facts About Mortgage Investment Corporation Shown

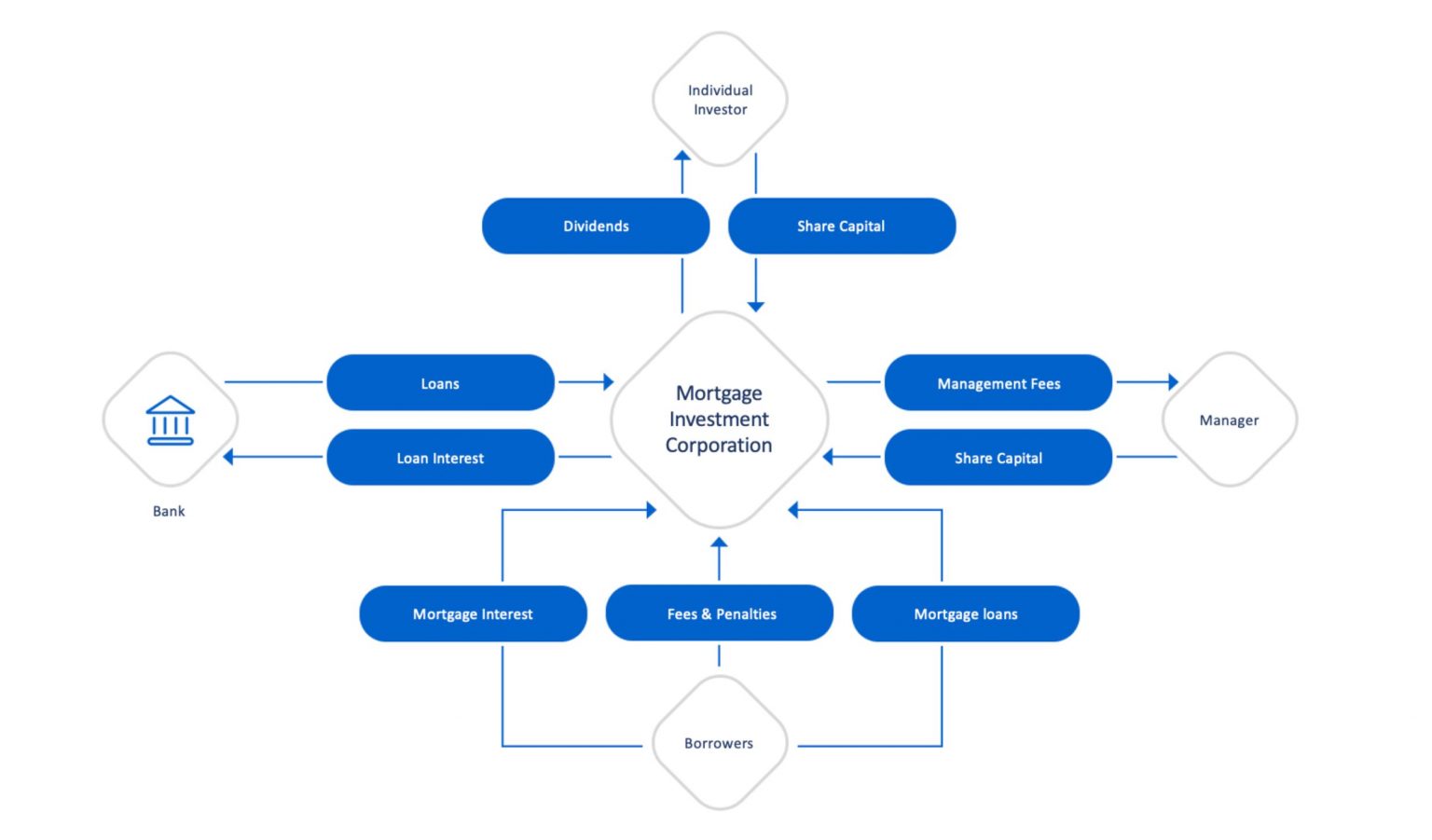

Does the MICs debt board evaluation each home loan? In most scenarios, mortgage brokers take care of MICs. The broker should not act as a participant of the credit history board, as this puts him/her in a straight conflict of rate of interest offered that brokers normally gain a compensation for placing the home mortgages.Is the MIC levered? Some MICs are levered by a banks like a legal bank. The banks will approve specific home mortgages possessed by the MIC as security for a credit line. The M (Mortgage Investment Corporation).I.C. will certainly then borrow from their credit line and provide the funds at a higher price.

It is crucial that an accounting professional conversant with MICs prepare these statements. Thank you Mr. Shewan & Mr.

Mortgage Investment Corporation - An Overview

This does not imply there are not risks, but, generally talking, regardless of what the wider securities market is doing, the Canadian property market, specifically significant cities like Toronto, Vancouver, and Montreal does well. A MIC is a company formed under the rules lay out in the Earnings Tax Act, Area 130.1.

The MIC gains revenue from those home mortgages on passion fees and general charges. The genuine allure of a Home mortgage Investment Company is the return it supplies financiers compared to other fixed income investments. You will have no problem discovering a GIC that pays 2% for a 1 year term, as government bonds are similarly as low.

Getting My Mortgage Investment Corporation To Work

A MIC should be a Canadian corporation and it should spend its funds in mortgages. That said, there are times when the MIC ends up owning the mortgaged residential property due to repossession, sale arrangement, and so on.

A MIC will certainly make interest income from mortgages and any money the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to investors, the MIC does not read the full info here pay any type of revenue tax obligation. As opposed to the MIC paying tax on the rate of interest it gains, shareholders are accountable for any type of tax obligation.

MICs issue usual and preferred shares, issuing redeemable recommended shares to shareholders with a taken care of returns rate. Most of the times, these shares are thought about to be "certified investments" for deferred income strategies. This is optimal for investors that acquire Home mortgage Financial investment Firm shares with a self-directed authorized retirement financial savings plan (RRSP), signed up retired life earnings fund (RRIF), tax-free savings account (TFSA), delayed profit-sharing strategy (DPSP), signed up education savings strategy (RESP), or signed up handicap financial savings strategy (RDSP).

And Discover More Here Deferred Strategies do not pay any kind of tax on the rate of interest they are estimated to get. That claimed, those who hold TFSAs and annuitants of RRSPs or RRIFs might be hit with certain penalty tax obligations if the financial investment in the MIC is thought about to be a "prohibited investment" according to Canada's tax obligation code.

Fascination About Mortgage Investment Corporation

They will ensure you have discovered a Home mortgage Financial investment Corporation with "competent financial investment" condition. If the MIC qualifies, it might be very valuable come tax obligation time considering that the MIC does not pay tax obligation on the interest earnings and neither does the Deferred Strategy. Mortgage Investment Corporation. Much more extensively, if the MIC stops working to satisfy the requirements established out by the Revenue Tax Act, the MICs earnings will certainly be taxed prior to it gets distributed to shareholders, reducing returns substantially

It shows up both the realty and securities market in Canada are at perpetuity highs At the same time yields on bonds and GICs are still near record lows. Also cash money is shedding its allure since energy and food costs have pressed the rising cost of living price to a multi-year high. Which pleads the concern: Where can we still find value? Well I believe I have the answer! In May I blogged concerning checking into home loan financial investment corporations.

The Definitive Guide for Mortgage Investment Corporation

If interest prices increase, a MIC's return would additionally boost since higher home mortgage rates suggest even more profit! MIC capitalists just make money from the excellent placement of being a loan provider!

Numerous effort Canadians that want to buy a residence can not get home mortgages from standard banks because maybe they're additional resources self utilized, or don't have a recognized credit report yet. Or possibly they want a short-term lending to establish a huge residential property or make some renovations. Banks have a tendency to disregard these possible customers because self utilized Canadians don't have steady revenues.